With 117 traffic accidents per day in 2025 and 288 fatalities that year (a rise of nearly 30% compared to 2024), the question is not whether you will ever be involved in a traffic accident in BiH, but when. This guide covers the complete procedure, from the first seconds at the scene to the insurance payout, including all deadlines, documents, and rules specific to Bosnian-Herzegovinian drivers in 2026.

This guide was prepared by the Auto Gas Gaga workshop in Banja Luka, drawing on years of experience with post-accident vehicles and pre-purchase inspections.

Table of Contents

- The First Five Minutes After a Crash

- When Police Are Required and When They Are Not

- When You Can Move the Car and When You Cannot

- The European Accident Report and How to Fill It In

- Photos and Evidence You Need at the Scene

- Filing an Insurance Claim: Deadlines and Documents

- Comprehensive vs Liability Insurance: Who Files Where

- What If the Accident Happens Abroad

- Most Common Mistakes BiH Drivers Make After a Crash

- Frequently Asked Questions

- Related Articles

The First Five Minutes After a Crash

The first five minutes are the most critical five minutes of the entire process. What you do or fail to do in that brief window determines how the rest unfolds, from the police report to the final insurance payout. The statistics are unforgiving: in 2025 BiH recorded a total of 42,762 traffic accidents, with July being the deadliest month in the Federation of BiH at 23 fatalities, while August had the highest overall accident count (2,818 in FBiH alone). The largest age group among traffic fatalities was 25-64, accounting for 41.7% of all victims.

Immediately after the collision, switch off the engine and turn on your hazard lights. Put on your reflective vest before stepping out of the vehicle, without exception, even in broad daylight on a clear, open road. Place the warning triangle 50 metres behind the vehicle on roads outside built-up areas, and 150 metres on a motorway or dual carriageway. At night or in fog, add another 50 metres. This is a legal obligation, but also a practical safeguard against being hit by oncoming traffic, especially on sections with limited visibility.

Check whether anyone is injured. If so, call the Emergency Medical Service immediately on 124 and do not move injured persons unless they face an immediate threat from fire or another oncoming hazard. If everyone is unharmed and there are no serious injuries, move on to documenting the accident.

Under Article 158 of the Law on the Fundamentals of Road Traffic Safety in BiH, drivers are obliged to exchange information immediately, complete and sign the European Accident Report, and photograph the scene. The law is clear: a driver must not leave the scene until these obligations have been fulfilled. Violating this provision carries misdemeanour liability and can seriously jeopardise your right to compensation.

When Police Are Required and When They Are Not

Many drivers automatically call the police after every contact, including a scratch in a car park. In practice, police attendance is not required in every situation, and a patrol may take several hours to arrive, particularly in smaller towns or at weekends.

You are required to call the police in the following situations. When there are injured persons, regardless of the severity of the injury. When material damage is significant or the parties cannot agree on liability. When one of the vehicles is foreign-registered. When any party lacks valid insurance or registration. When any driver is under the influence of alcohol or drugs. And when there is a suspicion of criminal activity, such as a stolen vehicle or forged plates.

When nobody is injured, both vehicles are registered and insured in BiH, the damage is minor, and both parties agree on what happened, filling in the European Accident Report and exchanging details is sufficient. This saves time and resources for both you and the police.

Failing to call the police when legally required can have serious legal consequences, including misdemeanour liability and problems with exercising your rights through the insurer. Given the recent amendments to traffic regulations in BiH, including the reckless driving law that came into force in 2026, the law is imposing increasingly strict penalties for non-compliance with post-accident procedures.

In the Federation of BiH, for roadside assistance call BIHAMK on 1282 (up to 3 free services per year for vehicles registered in FBiH). In Republika Srpska, call AMSRS on 1285 for the same purpose; they operate a 24/7 duty service. These services provide technical assistance and towing, not police intervention. For a detailed overview of all roadside assistance services in BiH, see our dedicated guide.

When You Can Move the Car and When You Cannot

This is one of the questions that causes the most confusion at the scene. The law states that you are obliged to remove vehicles from the roadway if they are obstructing traffic, but only on the key condition that you have documented everything first.

You may and are obliged to move vehicles off the roadway when nobody is injured, when you have photographed the position of both vehicles and any skid marks, when you have ideally marked the tyre positions on the road surface with chalk or another means, and when the passage for other traffic is blocked or seriously impeded.

You must not move vehicles until the police arrive in two cases: when there are injured persons, because the vehicle positions form part of the investigation and accident reconstruction, and when you have been unable to document the positions because you have no phone or other means of recording.

On a motorway or dual carriageway, regardless of the circumstances, the priority is the safety of the living. If you can, pull over to the hard shoulder. If you cannot move the vehicle, get out and take cover behind the crash barrier, as far from the roadway as possible. A motorway is the most dangerous place to stand beside a broken-down vehicle, because vehicles behind you are travelling at high speed and have limited time to react.

A practical tip that will never let you down: before moving either vehicle, take 20-30 photographs from every angle, including a wide shot showing both vehicles, the surrounding road signs, and the road surface condition.

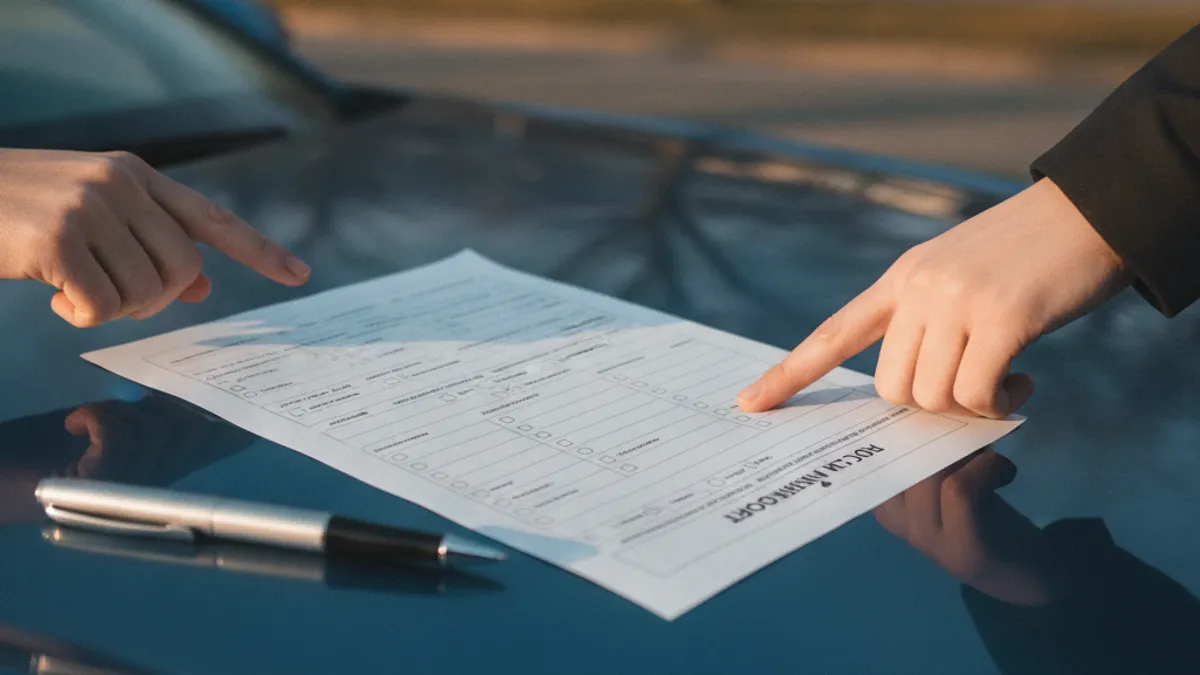

The European Accident Report and How to Fill It In

The European Accident Report (also known as the blue form) is a standardised document valid across Europe. A single form is completed by both parties simultaneously, and each party keeps one copy thanks to the carbon paper inside the form.

You can obtain the form from your insurer free of charge when taking out or renewing your policy, at a vehicle inspection station, or you can download and print it from the internet. Keep at least two blank copies in the car alongside your other documents, because you never know when you will need one. Fill it in exclusively with a ballpoint pen, as ink does not smudge in the rain and does not fade in the sun, unlike a pencil or felt-tip marker.

The form is completed in the following order. Top section: enter the date, time, and exact location of the accident, including the street name, number, and town. Side A and Side B: each party fills in their side with vehicle details (make, model, registration number), insurance details (insurer name, policy number, validity period), and driver details (name, surname, driving licence number, address, contact phone number).

In box 12, indicate the circumstances of the accident by selecting from the given options: reversing, pulling out of a parking space, turning, failure to give way, driving on the wrong side of the road, and so on. Tick every item that applies to your situation. In box 13, mark the point of impact on the schematic diagram of the vehicle.

How to Fill In Box 14 of the European Accident Report

Box 14 is the most important and most frequently incorrectly completed box on the entire form. In it you draw a sketch of the accident that serves the expert and the court as a visual representation of what happened.

Draw the roads or carriageway with arrows showing the direction of travel of both vehicles before the collision. Label the vehicles A and B, corresponding to the sides of the form. Draw the position of both vehicles at the moment of contact. Mark any traffic signs, traffic lights, and road markings relevant to establishing liability, such as a stop sign, solid line, traffic light, or give-way sign. Mark the exact point of contact on both vehicles.

You do not need to be an artist. A clear diagram with arrows, letter labels, and one or two notes is perfectly sufficient. The judge or expert who reads your report is looking for clarity and precision, not aesthetics.

Signing the European Accident Report only confirms that the facts described in the report are accurate as stated on your side of the form. A signature does not constitute an admission of liability or guilt, which is one of the most widespread misconceptions among drivers. Who is at fault is determined subsequently, on the basis of all evidence gathered: the sketch, witness statements, physical traces, and potentially expert analysis. Many drivers refuse to sign the report precisely because of this misconception, thereby creating a bigger problem for themselves, since an unsigned report carries significantly less evidential weight with insurers.

Photos and Evidence You Need at the Scene

The phone in your pocket is your most important tool at the scene of an accident, second only to the warning triangle and reflective vest. The documentation process described here takes a total of ten minutes and can save you weeks of wrangling with the insurer.

Photograph the following, in this order of priority. A wide shot of both vehicles in the position they were in at the time of the accident, before any movement whatsoever. Close-up shots of the damage on both vehicles, each area of damage from at least two angles. The registration plates of both vehicles (legible). Skid marks on the road surface, if present. Traffic signs and traffic lights in the immediate vicinity. The road surface condition (wet, dry, ice, pothole, mud or gravel deposit). The surroundings (lighting, visibility, obstructions to the line of sight). And the insurance policy and driving licence of the other party.

Also record a short video of 30-60 seconds, slowly circling both vehicles. Video captures spatial information that static photographs lose, particularly the three-dimensional relationship between the vehicles, the road surface, and the surroundings.

All photographs taken with a modern phone automatically have the time and GPS coordinates embedded in the EXIF data. This is digital evidence that is very difficult to dispute before a court or insurer, because it contains independent confirmation of when and where the photograph was taken.

If there are witnesses, ask them for their name, surname, and contact phone number. A witness who saw the accident from the pavement or from another vehicle can be a decisive factor if the proceedings become complicated and end up in court.

Filing an Insurance Claim: Deadlines and Documents

The clock starts ticking from the moment of the accident and waits for no one. The standard deadline in practice for filing an insurance claim is 15 days from the date of the accident. This deadline is a regional convention in BiH and may vary depending on the entity and the specific policy terms, but 15 days is the standard observed by the vast majority of insurance companies in both entities.

To file a claim, prepare the following documents: the completed and signed European Accident Report (your copy), all photographs and video recordings from the scene, the police report if the police attended the scene, a copy of your vehicle registration certificate, a copy of your driving licence, a copy of your insurance policy, and the completed claim form obtained from the insurer.

Insurance Claim Deadlines in BiH

The deadlines for claim settlement by the insurer are legally defined and binding on the insurer. For minor material damage up to the equivalent of EUR 1,000, the insurer is obliged to resolve the claim within 8 days of a properly submitted application with complete documentation. For larger material claims, the deadline is 45 days. For non-material claims, which include physical pain, fear, and emotional distress, the deadline is 90 days.

If the insurer exceeds these deadlines, you have a legal right to statutory default interest for the period of delay. You also have the right to engage an independent court-appointed expert for damage assessment if you believe the insurer's valuation is too low or unfounded. The costs of an independent assessment can be claimed from the insurer if their valuation proves to have been unjustifiably low.

Comprehensive vs Liability Insurance: Who Files Where

The difference between liability insurance (AO - auto-odgovornost, compulsory by law) and comprehensive insurance (kasko, voluntary, extended cover) determines who you file with and what you can realistically expect as an outcome.

Liability insurance covers the damage you cause to someone else, but does not cover damage to your own vehicle. So if you are at fault, the injured party files a claim with your insurer, who compensates them. Your car is not repaired under a liability policy - only the other party's car is. That is why liability insurance is compulsory by law and why every registered vehicle owner in BiH pays for it.

Comprehensive insurance covers your own car regardless of who is at fault. If you have comprehensive cover and you are at fault, your comprehensive insurer repairs your car, less the excess (deductible). If you are not at fault, you have two options: file with your own comprehensive insurer (faster resolution, but you pay the excess) or file against the at-fault party's liability insurer (slower, but at no cost to you).

If you have comprehensive insurance, submit a claim to both your comprehensive insurer and the at-fault party's liability insurer simultaneously. Comprehensive cover usually resolves claims considerably faster, and your insurer will itself seek reimbursement from the at-fault party's liability insurer through subrogation. You do not have to wait, and you do not have to run a parallel process.

The worst-case scenario: you are not at fault, you have no comprehensive cover, and the at-fault party has no valid liability insurance. Even then there is a legal remedy. You pursue the claim directly against the at-fault party through a civil lawsuit, and the BiH Insurance Protection Fund covers claims arising from uninsured and unidentified vehicles, although only for bodily injuries and third-party damage up to the statutory minimum coverage.

What If the Accident Happens Abroad

It is summer, you are packing the car and heading to the coast or on a road trip across Europe. An accident on a Croatian or Montenegrin motorway is just as likely as one at home, and the procedure has its own specific rules that you need to know in advance, before you get behind the wheel.

BiH drivers do not need to carry a Green Card for the 38 signatory countries of the Green Card system, including all EU member states, Serbia, Montenegro, and most other European countries. Your liability insurance policy is automatically valid in all of these countries, meaning you are covered from the moment you cross the border without any additional document.

However, a Green Card is compulsory for 8 countries and you must purchase one from your insurer before departure: Albania, Azerbaijan, North Macedonia, Morocco, Moldova, Tunisia, Turkey, and Ukraine. Without a Green Card in these countries, you are not only uninsured but also risk problems at the border crossing.

Accident in Croatia as a BiH Driver: What to Do

Since Croatia is the most popular destination for BiH drivers in summer, here is a concrete step-by-step procedure. Call the European emergency number 112, which operates in all EU countries and combines police, emergency medical services, and the fire brigade. Fill in the European Accident Report at the scene, since it is the same standardised form you use in BiH. Request a police report if police intervention was necessary. Upon returning to BiH, file a claim with your insurer within the standard 15-day deadline.

If you are the injured party and the at-fault driver has foreign plates, you can also file the claim in BiH through the claims settlement representative (correspondent) of the at-fault party's insurer in BiH. Information on who the correspondent is can be obtained from the BiH Green Card Bureau. This system exists precisely so that you do not have to pursue proceedings in a foreign country, in a foreign language, and under foreign regulations.

Keep every piece of paper you receive abroad without exception, including receipts for towing, accommodation, medical examinations, medication, or temporary vehicle repairs. These are all documented costs that can be claimed from the at-fault party's insurer.

Before every trip abroad, check that you have everything legally required in the car: a warning triangle (some countries require two), a reflective vest for every occupant, a first-aid kit with a valid expiry date, a spare wheel or repair kit, at least two blank European Accident Reports, and a Green Card if required. For a detailed list of mandatory equipment by country, see our complete guide to driving from BiH in 2026.

Most Common Mistakes BiH Drivers Make After a Crash

Based on experience with vehicles arriving at the workshop after collisions and conversations with their owners, these are the mistakes that recur year after year.

Admitting fault at the scene. Under stress and adrenaline, many people say "sorry, it was my fault" before they have even taken in the full picture. That informal statement can be used against you in subsequent liability proceedings. Be courteous, help if someone is injured, but do not accept blame until all the evidence is on the table.

Not photographing before moving the vehicles. Once you move the car from the point of impact, the original position is lost forever. Without photographs, anyone can claim anything, and the insurer has no reliable basis for an objective assessment of the circumstances.

Filling in the European Accident Report at home. The report is to be completed at the scene, while memories are fresh and both parties are present. Completing it later opens the door to disagreements, alterations, and accusations of document falsification.

Missing the deadline for filing a claim. If you file your claim after the standard 15-day period has expired, the insurer may reject the claim or significantly complicate the processing. As soon as you get home from the scene, call the insurer and start the claim the same day.

Repairing the vehicle before the damage assessment. If you take the car to a garage and repair it before the insurer's assessor has inspected and documented the damage, you forfeit your right to compensation for that amount. The assessor must see the actual condition of the vehicle, not the already-repaired state.

Signing a settlement without consideration. Insurers sometimes offer a quick settlement that is significantly below the actual market value of the damage, counting on you accepting out of impatience or ignorance. You have a legal right to a second independent assessment and to engage a court-appointed expert. Do not sign anything under pressure or with less than a few days to think it over.

Nobody plans an accident, but preparation is the difference between a chaotic experience and a controlled procedure with clear steps. Print the checklist from this guide and put it in the glove box. Buy two blank European Accident Reports from your insurer and keep them with the documents in the car. Check that your insurance policy is valid and that you know the contact details of your insurance company.

If you need a vehicle inspection after an accident or an assessment of mechanical damage, get in touch via the contact page or book an appointment directly.

Frequently Asked Questions

What is the deadline for reporting a traffic accident to the insurer in BiH?

The standard deadline in practice is 15 days from the date of the accident. This is a regional convention and may vary depending on the entity and the specific insurer, but 15 days is observed by the vast majority of insurance companies in BiH. Do not wait until the last day - file your claim as soon as possible, because delay can be grounds for rejection.

Does signing the European Accident Report mean I am admitting fault?

No. The signature only confirms that the facts in the report are accurate as stated on your side of the form. Who is at fault is determined subsequently, on the basis of evidence, the sketch, witness statements, and potentially expert analysis. An unsigned report carries less evidential weight and can complicate proceedings with the insurer.

When is the European Accident Report sufficient without calling the police?

When nobody is injured, both vehicles are registered and insured in BiH, the damage is minor, and both parties agree on the circumstances of the accident. In all other situations (injuries, a foreign vehicle, an uninsured party, alcohol, disagreement over fault) the police are required.

How quickly must the insurer pay out a claim?

For minor material damage (up to the equivalent of EUR 1,000) the deadline is 8 days from a properly submitted claim. For larger material claims the deadline is 45 days, and for non-material claims (pain, fear, emotional distress) the deadline is 90 days. If the insurer exceeds these deadlines, you have a right to statutory default interest.

Do I need a Green Card to drive to Croatia?

No. A BiH liability insurance policy is automatically valid in Croatia and in a total of 38 signatory countries of the Green Card system, including all EU member states, Serbia, and Montenegro. A Green Card is compulsory only for 8 countries: Albania, Azerbaijan, North Macedonia, Morocco, Moldova, Tunisia, Turkey, and Ukraine.

What should I do if the at-fault party has no insurance?

You pursue the claim directly against the at-fault party. The BiH Insurance Protection Fund covers claims arising from uninsured and unidentified vehicles, but only for bodily injuries and third-party damage up to the statutory minimum. For material damage to your vehicle caused by an uninsured at-fault party, the legal route is a civil lawsuit.